Follow

Follow Get in touch

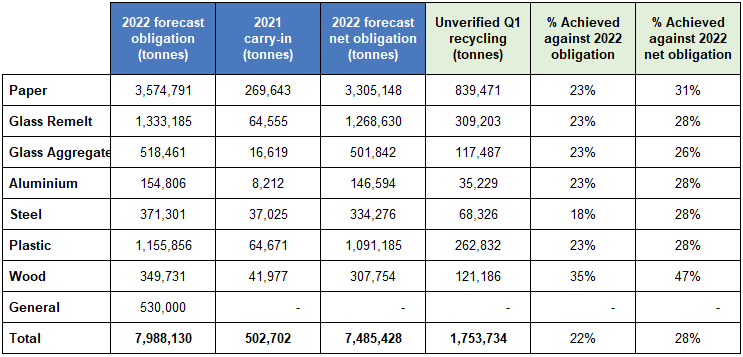

The Q1 unverified recycling figures released by the Environment Agency indicate that only one material would have hit the quarterly target without carry-in.

The table below shows estimated gross and net requirements for 2022 packaging recycling. It also shows the carry-in tonnage reported earlier in the month. Carry-in is the amount of PRNs produced in December 2021 that are issued for 2022 use, with the amount increasing in comparison to the previous year, most significantly in plastic.

When we take carry-in into account, all materials are performing well against the recycling targets, showing a surplus in all materials.

What does the data mean for producers?

Without carry-in, recycling volumes across all materials (bar wood) have not met the minimum 25% recycling target. Whilst the data is unverified and we expect the volumes for some material to increase over the coming weeks, this is not a very positive start to the year.

There will be an immediate price correction across all materials and prices will rise in the short term until we receive the UK demand, which should be issued by mid-May.

Plastic - High risk

Plastic recycling has had a slow start to the year and only saw a slight uplift last month due to higher PRN prices. The export data is significantly reduced compared to last year, as exporters face export problems into Europe, tighter EA accreditation requirements and shipping concerns due to the Ukraine situation.

Whilst the data is unverified and we wait for the UK demand to be published, the market has already reacted to the news and prices have started to increase. We expect prices to continue to rise until mid-May when demand will be published.

Steel - High risk

Steel recycling has only achieved an estimated 18% of its recycling target and the market would expect a minimum of 25% at this point in the year. The steel recycling target is heavily reliant on exports and with the increasing costs of shipping containers, issues shipping into Europe and the tighter controls the EA have imposed on exporters, the Q1 data was a surprise to the industry.

The UK volume remained lower than expected due to one UK recycler not applying for their accreditation until recently. PRN prices have started to rise and will continue to until the monthly data shows an increase in recycling.

Paper - Medium risk

Paper recycling has seen a slow start to the year, whilst the OCC prices have remained high the PRN price has remained extremely low and has deterred recyclers from claiming the PRN.

A price increase is needed to ensure that recyclers continue to claim the PRN. Any further slowdown in paper recycling will impact general recycling although at this point in the year it is not a concern.

Aluminium - Medium risk

Recycling volumes continue to remain strong during the first quarter of the year, and the carry out data was also inline with the previous year.

The only threat to aluminium is an increase in the placed on the market data which will not be known until mid-May, as brands move away from plastic packaging and some are moving to aluminium demand could increase over and above the recycling target. PRN prices will stabilise at the current levels until demand is known.

Glass - Medium risk

Glass recycling volumes remain low for the start of the year, whilst the carry-in remelt PRN volumes were better than expected. Aggregate recycling has also reduced over the last few months which has led to immediate price increases in both PRNs.

Whilst we await the UK demand data, PRN prices will continue to increase, although there is a risk that demand could be significantly lower than last year.

Wood - Low risk

Wood is well on its way to meeting its recycling target, having achieved 35% already. The UK requires wood recyclers to continue to produce PRNs to support the general recycling target, especially as paper is tracking slightly behind its recycling target. There is a slight risk that prices will increase, following the same trend as paper.

Looking ahead

Ecosurety will continue to communicate the changes in the PRN market throughout the year. Whilst the start of this year is not what the market expected, it is important that we await the demand data which is due to be published mid-may.

If you would like to speak with our team, please contact us on 0333 4330 370.

Sandeep Attwal

Group procurement manager

Sandeep works in the role of Group procurement manager. Sandeep builds and maintains strategic relationships with our key service partners for packaging, batteries and WEEE, whilst creating new relationships and initiatives to improve UK recycling. Sandeep has over 17 years’ experience of the regulations and understands the challenges and opportunities that can arise from volatile markets.

Written by

Sandeep Attwal

Published

26/04/2022

Topics

Latest News

Q2 2024 recycling data shows strong performance in H1

By Sam Marshall 24 Jul 2024

Ecosurety continue to step up for refill and reuse

By Victoria Baker 24 Jun 2024

Ecosurety renews B Corp™ certification with flying colours

By Louise Shellard 11 Jun 2024

Ecosurety sponsor the 2024 Carbon Literate Organisation Awards

By Louise Shellard 07 Jun 2024